CzechInvest Information Series No. 1

Serial No.: INV/1/95-1

Date of Issue: January 1, 1995

Investors expect governments to create a stable political and economic environment and that is exactly what has happened in the Czech Republic the country's level of stability, both political and with regard to rapid liberalisation and privatisation, has no parallel in any of the post communist countries. Launched on January 1, 1991, the Czechoslovak economic reform has aimed to re-integrate the national economy with those of the developed world market through privatisation, the liberalisation of prices and foreign trade, the establishment of internal currency convertibility, macro economic stabilisation, and the attraction of foreign direct investment (FDI).

Repatriation of Profits and Capital

With the government of Czech Prime Minister Vaclav Klaus able to rely on a strong pro-reform consensus, the Czech Republic (CR) enjoys a high level of political stability. Opinion polls show that Klaus' Civic Democratic Party, closely identified with the political and economic reforms of the last four years, still commands strong support. The government currently holds a firm 53% majority in parliament, with the next elections scheduled for 1996.

In a March 1994 survey of Eastern Europe and the former Soviet Union conducted by Ernst and Young and World Link, the CR received a perfect score for overall political and economic stability, outranking all other countries surveyed.

Having already installed the essential legal and institutional framework, the government is now focusing its efforts on reorienting its economy toward the European Community market, which currently represents over 50% of the country's trade.

The CR's conservative fiscal policies have produced a stable and reliable investment climate with the lowest level of inflation in central and eastern Europe, strong foreign currency reserves, the region's lowest foreign debt per capita, and favourable exchange rates. Strict economic policies have sought to achieve a balanced budget, with an independent central bank controlling the money supply.

Inflation rates have continued to decrease after the high 20.8% 1993 average inflation rate caused by introduction of the value-added tax (VAT) in January 1993. Inflation fell to 9.3% in May 1994 (compared to one year earlier), and average inflation for 1994 is estimated to be 10.3%. Forecast for 1995 is about 9%.

The CR's US $852 national debt per capita is the region's lowest, much less than its nearest competitor, Hungary (with a per capita debt of $2,150). This low national debt illustrates the Czech government's rejection of such short-term measures as higher borrowing, which has increased national debt in many Western economies.

Such economic policies have led to improved ratings from Moody's Investors' Service and Standard a Poor's, making the CR the first post-communist country to be rated, respectively, Baa2 and BBB+.

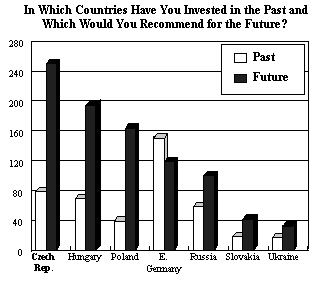

In a survey of senior executives attending the European Chairmen's Symposium in Berlin (July 1993) conducted by The Wall Street Journal Europe, MPG International, and the German newspaper Handelsblatt, the CR surpassed its Central and East European neighbours to receive the executives' highest vote of confidence . The CR was overwhelmingly voted as having the region's best economic prospects, as well as being the most attractive country for future investment (see table). The Czech workforce was also ranked best by almost half of the voters, well ahead of eastern Germans, Hungarians, Poles and Russians.

In Which Countries Have You Invested in the past

and Which Would You Recommend for the future?

Note: numbers represent scoring system used when executives were asked, first, in which countries they had already invested and, second, which they considered most attractive for future investment. Six points were given to each executive's largest investment or preference, five points to the second-largest, etc. Source: MPG International / Wall Street Journal

The inflow of foreign direct investment (FDI) reached almost US$2.7 billion by October 1, 1994, increasing more than 500% within the last three years. The most common forms of FDI are:

- joint ventures - to date, joint ventures with recently privatised companies have been the dominant form of foreign investment;

- greenfield investments;

- participation in the privatisation process - although the deadline for submitting projects for the second wave of privatisation has passed, many approved projects have been designed to accommodate future foreign investors.

Investors can also acquire equity positions through the Prague Stock Exchange.

Czech legislation enables foreign entrepreneurs to conduct business in the CR under the same conditions as Czech entrepreneurs. A foreigner may become either the sole or co-founder of a company, and may also join an existing Czech enterprise. Foreigners who own businesses abroad may also conduct business activities in the CR provided they own a branch office within the CR.

According to the Czech Commercial Code, the official forms of business entities accepted by the Commercial Register include: joint-stock; limited liability; limited partnership; unlimited partnership; co-operative; silent partnership; and branch office of a foreign company.

There is no upper limit on the level of foreign investment in the CR.

NOTE: For more detailed information, please refer to fact sheets no. 8, "Setting Up a Business in the Czech Republic," and no. 3, "Privatisation in the Czech Republic."

Foreign entrepreneurs can make use of credits granted by both Czech and foreign banks.

As in other countries, interest rates vary according to the duration of credit, and are expected to decrease along with future economic development. Czech banks offer short-term (up to one year), medium-term (1-4 years) and long-term (over four years) credits.

The protection of foreign investments is guaranteed through a number of intergovernmental agreements signed by the former Czech and Slovak Federal Republic (CSFR) and approximately 30 other countries; the CR continues to honour all such agreements.

To engage in trade, entrepreneurs must apply to the respective trade office for authorisation. This may come as a trade certificate or a trade license, depending on the nature of the business.

Persons having a domicile or seat outside the CR must also establish a responsible representative to act in compliance with trade regulations.

On January 1, 1991 internal convertibility of Czechoslovak currency was guaranteed under the Foreign Exchange Act, enabling entrepreneurs to buy foreign currency from Czech financial institutions for payment of imports.

Entrepreneurs are obliged to offer all convertible currencies to the banks (except cash contributions to stock capital and foreign currency deposits into foreign exchange accounts) but at the same time have guaranteed access to convertible currencies.

The exchange rate is now fixed between the Deutsch mark and the U.S. dollar. A very significant foreign currency deposit scheme, with extensive double taxation agreements running with most major countries, readily facilitates international trade.

REPATRIATION OF PROFITS AND CAPITAL

Czech foreign exchange regulations and investment protection agreements guarantee the transfer of profits and capital abroad.

When requested by businesses, Czech banks must pay foreign investors foreign currency equivalent to their return on invested capital in Czech currency. This includes cash earnings from domestic investment mainly entrepreneurial profits, interests, capital gains, return on securities, and royalties.

The current taxation system, introduced in January 1993, includes a value-added tax (VAT) of 5% for services and 23% for goods, similar to those in most Western European countries.

Businesses in the Czech Republic are subject to a corporate income tax of 41%, regardless of total income. Special tax rates are set for certain types of income (i.e. a rate of 25% for income derived from commercial, engineering or other consulting services, intermediary services rendered in the country by taxpayers having a seat outside the CR, and earnings derived from the transfer and use of industrial property rights).

Those living in the Czech Republic for at least 183 days in one calendar year are subject to a personal income tax. Tax rates vary according to annual income, ranging from 15-44%.

Future tax reform will result in a reduction of direct taxes paid by companies as the Czech government aims at shifting the tax burden away from enterprise onto indirect taxation.

NOTE: For more information, please refer to fact sheet no. 4, "Taxation in the Czech Republic."

Prices were liberalised in the former CSFR on January 1, 1991. Currently, only 5% of prices are regulated, (i.e. water, certain medications and health care equipment, solid fuels).

As a founding member of GATT (the General Agreement on Tariffs and Trade), the CR applies import duties according to the valid and internationally recognised customs tariff.

As of July 21, 1993 joint venture or limited liability companies in the CR with at least 30% foreign ownership (equalling no less than US$1.7 million) are allowed one year of exemption from customs duties on raw materials or semi-processed goods imported through the foreign partner for furthers manufacturing in the CR. The law, intended to encourage new companies, is valid for established enterprises until July 1994 or, in the case of new enterprises, for one year after their foundation. As a pro-export measure the law also requires companies to then export an amount of the resulting manufactured goods whose value at least equals that of the imported materials. The law is valid until the end of 1996.

Also exempt from import duties are certain selected types of goods, goods not subject to customs clearance (for personal use by diplomats, members of government, etc.), and goods located in customs-free zones and storehouses.

A significant attraction for foreign investors is the highly cost-effective Czech labour force. Average wage rates , according to JP Morgan's Emerging Markets Economic Weekly , are 13.5% and 40.5% lower than in Poland and Hungary, respectively.

Employer "on costs" (i.e. payments for social security and health insurance funds), according to Price Waterhouse, are 25% and 32% lower than in Poland and Hungary, respectively.

With an outstanding 1991 literacy rate of 98.9%, the Czech workforce is educated, skilled, and was ranked the highest in Eastern Europe, surpassing Hungary in measures of managerial skills. According to a December 1993 OECD report on education, the CR produces a higher percentage of science and engineering graduates than any other country in the world.

Foreign citizens may be employed in Czech companies provided they acquire a work permit from the respective labour office and a residence permit from either the diplomatic or consular office of the CR abroad, or from the Ministry of the Interior in the CR.

NOTE: For more information, please refer to fact sheet no. 10, "Labour and Social Policy."

NOTE: This information is current as of January 1995. Although we have made every effort to ensure the reliability of our sources, CzechInvest does not assume responsibility for its accuracy.